Your credit score affects many parts of your life—from getting loans to renting an apartment. Yet most people don’t fully understand how credit scores work or what influences them. The good news? Improving your score is easier than you think once you understand the basics.

Why Credit Scores Matter

A strong credit score makes life easier. It opens doors to better loans, lower interest rates, and financial opportunities that can save you thousands over your lifetime.

How a Good Score Benefits You

With a good credit score, you’re seen as a responsible borrower, which makes banks and lenders more willing to trust you.

What Is a Credit Score?

Definition and Purpose

A credit score is a three-digit number that shows how trustworthy you are when it comes to borrowing money. It helps lenders decide whether to approve your loan applications.

How Credit Scores Are Calculated

Scores are based on several factors like your payment history, credit usage, and more.

Components of a Credit Score

Payment History

This is the biggest factor. Paying on time boosts your score; missing payments hurts it.

Credit Utilization

How much of your available credit you use. Keeping it under 30% is ideal.

Length of Credit History

The longer your credit accounts have been open, the better.

New Credit Inquiries

Multiple applications for credit can lower your score.

Credit Mix

Having different types of credit—like credit cards, loans, etc.—strengthens your score.

Types of Credit Scores

FICO Score

The most widely-used scoring model.

VantageScore

Another popular model created by major credit bureaus.

Differences Between the Two

While both measure similar factors, weighting and scoring ranges may differ.

Why Credit Scores Are Important

Loan Approval

Lenders rely heavily on your score to approve or deny loans.

Better Interest Rates

Good scores mean lower interest rates, saving you money.

Renting a Home

Landlords often check credit to ensure you’ll pay rent on time.

Employment Opportunities

Some employers check credit reports when hiring for financial positions.

How Credit Reports Work

What’s in a Credit Report?

It includes your credit accounts, payment history, debts, and personal details.

Major Credit Bureaus

Experian, Equifax, and TransUnion.

How Often You Should Check Reports

At least once a year—more often if you’re rebuilding credit.

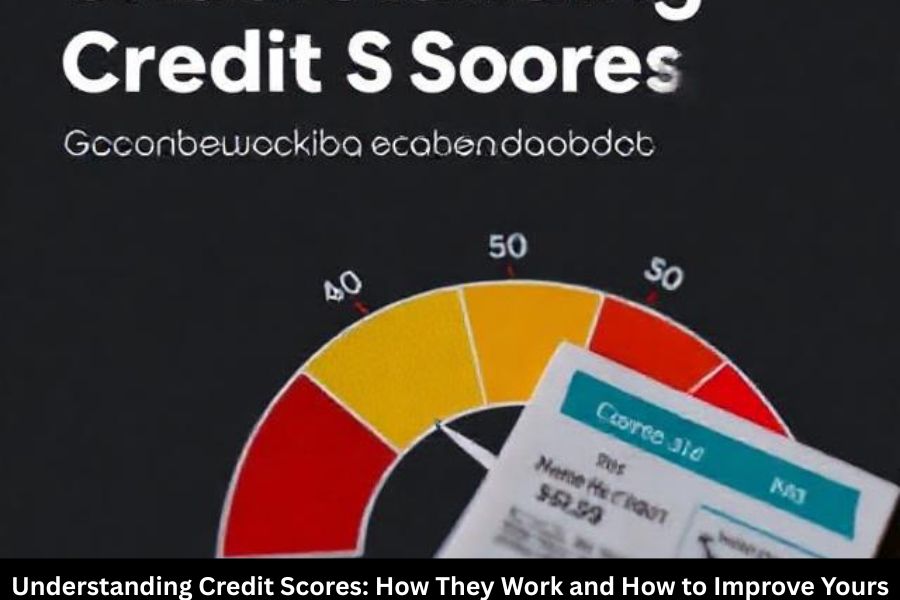

Common Credit Score Ranges

- Poor: 300–579

- Fair: 580–669

- Good: 670–739

- Very Good: 740–799

- Excellent: 800+

Reasons Your Credit Score Might Drop

Late Payments

Just one missed payment can significantly lower your score.

High Credit Utilization

Using too much of your credit limit signals risk.

Too Many Credit Applications

Each hard inquiry may drop your score a few points.

Errors on Your Credit Report

Incorrect information can damage your score if not corrected.

How to Improve Your Credit Score

Pay Bills On Time

Your payment history makes the biggest impact.

Lower Your Credit Utilization

Aim to use less than 30% of your total credit limit.

Avoid Opening Too Many Accounts

Space out your credit applications.

Diversify Your Credit Mix

A combination of installment and revolving credit strengthens your score.

Dispute Credit Report Errors

Fixing errors can instantly improve your score.

Smart Credit-Building Strategies

Use a Secured Credit Card

Perfect for beginners or those rebuilding credit.

Become an Authorized User

Benefit from someone else’s good credit habits.

Take Small Installment Loans

Such as credit-builder loans.

Keep Old Accounts Open

Older accounts help boost your average credit age.

Debunking Common Credit Score Myths

Checking Your Score Hurts It

False. Checking your own score is a soft inquiry and doesn’t affect it.

You Need Debt to Build Credit

You only need responsible credit usage—not debt.

Closing Accounts Helps Your Score

Closing accounts can actually lower your score.

Protecting Your Credit Score

Identity Theft Protection

Monitor accounts to prevent unauthorized activity.

Monitoring Accounts Regularly

Small issues caught early prevent big score damage.

Practicing Smart Financial Habits

Consistency is key to maintaining a strong score.

When to Seek Professional Help

Credit Counseling Agencies

They help you manage debt and build healthy habits.

Debt Management Plans

Professionals negotiate better terms with creditors.

Avoiding Scams

Be wary of services promising “instant credit fixes.”

Final Tips for Maintaining a Strong Credit Score

Be Consistent

Good habits over time create strong credit.

Review Your Finances Regularly

Stay aware of changes in your credit.

Stay Organized

Track bills, debts, and due dates.

Conclusion

Your credit score plays a vital role in your financial life, from securing loans to impacting your everyday opportunities. When you understand how it works, you can take control and improve it with simple, consistent steps. Whether you’re starting from scratch or rebuilding after setbacks, improving your credit score is absolutely achievable. Start today—your future self will thank you.

FAQs

How often should I check my credit score?

At least once a month is ideal.

Can I improve my credit score quickly?

Small changes like lowering utilization can improve your score in weeks.

Does paying off a loan help my credit?

Yes—it shows lenders you can manage debt responsibly.

Is it bad to have multiple credit cards?

Not if you manage them well and keep balances low.

Can credit report errors really hurt my score?

Absolutely. Even small mistakes can lower your score significantly.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://www.binance.com/register?ref=IXBIAFVY

дизайн бюро спб дизайн студия интерьера санкт петербург

Play online at https://elonbet-casino-game.com: slots, live casino, and special offers. We explain the rules, limits, verification, and payments to avoid any surprises. This material is for informational purposes only.

Нужен трафик и лиды? настройка контекстной рекламы в avigroup SEO-оптимизация, продвижение сайтов и реклама в Яндекс Директ: приводим целевой трафик и заявки. Аудит, семантика, контент, техническое SEO, настройка и ведение рекламы. Работаем на результат — рост лидов, продаж и позиций.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.com/cs/register?ref=OMM3XK51

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Visit Site – Layout is crisp, browsing is easy, and content feels trustworthy and clear.

actionable learning space – Provides insights that can be applied right away with little effort.

trusted link center – Easy to explore, with all relevant information organized clearly.

industry insight center – Helpful resources, analysis makes understanding market shifts simple.

business strategy portal – Clear explanations, applying ideas feels achievable.

click for practical tips – Content feels useful and offers direct, real-world applications.

click for market knowledge – Platform offers easy-to-digest insights for navigating current business trends.

natural progress guide – Very clear guidance, moving forward feels smooth and manageable.

discover new angles – Browsing here made it easy to think differently about next steps.

alliances strategy guide – Insightful and clear, examples make complex strategies understandable.

forward energy flowing – Gentle, approachable phrasing illustrating how liberated energy improves outcomes.

SmartDigitalShop – Clear categories and fast navigation improve the shopping experience.

LongTermGrowthGuide – Informative and actionable, spotting long-term opportunities is easy.

trustedmarketplace – Enjoy a smooth and secure shopping journey with confidence.

build valuable connections – Great explanations here, guidance feels practical and useful.

digitalecommercecenter – Smooth platform that makes purchasing products online effortless.

flowing goal strategies – Very actionable advice, helps maintain focus and reach outcomes successfully.

networkhub – Extremely useful, offers clear ways to build professional connections.

partnership insights platform – Very actionable, real-world examples illustrate alliance strategies well.

move forward clearly – Natural and motivating, illustrating how focus drives action.

CorporateInsightHub – Provides reliable corporate information in a clean, professional interface.

corporatealliancesguide – Clear and actionable, growth partnerships are easy to understand and implement.

EnterpriseFrameworkCenter – Practical and helpful, the platform makes enterprise frameworks easy to grasp.

dependableshopping – Smooth and secure online purchases with confidence every time.

ExploreIdeasPro – Fun and accessible explanations, innovations are presented clearly.

expand knowledge base – Feels motivating and well structured for gradual learning.

trusted connections hub – Very clear content, networking with peers is natural.

growthinsightsportal – Practical guidance that simplifies complex growth concepts.

businessboost – Practical and actionable, readers can implement ideas immediately.

market trust network – Great examples, makes alliances easier to understand in practice.

clarity solutions – Informative and actionable, breaks down ideas clearly.

SmartDecisionHub – Reliable tips, helps you weigh options clearly and make sound choices.

strategy with momentum – Gentle phrasing that emphasizes the flow of planned action.

valuealliances – Provides actionable insights for creating trustworthy and effective collaborations.

corporate networking guide – Great resource, connecting with enterprises is easy and professional.

nextlevelskills – Helpful learning hub, skills development tips are practical and clear.

DigitalCartPro – Easy-to-navigate, online buying is straightforward and quick.

checkouthub – Smooth and convenient, the platform makes online shopping easy.

trusted alliance resources – Informative content, helps relate alliances to practical business cases.

city shopper’s choice – Offers a well-curated selection that feels stylish and relevant.

ClearGrowthPlans – Practical ideas for growth that can be applied immediately.

attention accelerator – Great resource, learning how to focus improves efficiency significantly.

strategic signals – Gentle, motivating tone, highlighting that intentional signals guide progress smoothly.

tacticalinsights – Offers concise advice for taking practical steps toward business success.

strategic partnership hub – Practical tips, forming professional connections feels natural.

buyingcenter – Clear and efficient, platform makes purchasing online simple and convenient.

LongTermStrategyCenter – Structured guidance, long-term business goals are explained clearly.

safeshoppingdeals – Very convenient, shopping for deals online is intuitive and secure.

trusted partnership insights – Well-structured examples, makes alliance strategies easier to follow.

SecureCheckoutCenter – Practical and simple, completing purchases online is straightforward.

OutletForIdeas – Fun, creative site with clear layout, ideal for exploring concepts.

relationshiphub – Explore strategies to strengthen professional ties effortlessly.

enterprise bond help – Comes across as dependable with clear, calm explanations.

click to gain knowledge – Helpful lessons, concepts are explained in an understandable way.

modernshoppinghub – Simple and practical, the platform makes online purchasing easy and stress-free.

linkstrategy – Great resource, collaboration tips are both clear and actionable.

market partnership guide – Clear guidance, real examples make strategies understandable.

partnership growth network – Engaging and professional, suitable for long-term business partnerships.

QuickBuyPro – Makes shopping effortless with a clean and modern interface.

sustainable growth space – Offers actionable advice to maintain progress and growth over the long term.

practicaltipscenter – Offers useful insights that are easy to act on immediately.

KnowledgeStream – Educational platform, learning new ideas is intuitive and well-laid-out.

AttractResults – Practical guidance that leads to noticeable improvements in outcomes.

forwardshop – Informative and clear, platform explains retail trends in a practical way.

businessalliancesnetwork – Strong emphasis on corporate networking, feels credible and organized.

click for digital learning – Friendly tutorials, guides are structured and simple.

onlinestoreplus – Streamlined process, shopping online feels quick and reliable.

market alliance strategies – Clear advice, helps connect theory to practical market scenarios.

shop without hassle – Appears clean and structured to reduce unnecessary steps.

learning strategy platform – Encourages intelligent learning habits with a focus on scalable outcomes.

OptionClarityCenter – Offers practical tips to make strategy planning less overwhelming.

CostWiseShop – Highlights savings while maintaining a smooth online shopping experience.

growth planning hub – Provides explanations that are practical and supportive of future success.

bondingmasterplan – Offers guidance to navigate commercial bonds efficiently and securely.

learnfromexpertinsights – Excellent site, expert insights are practical and easy to apply today.

industrymastery – Clear and actionable, readers can implement strategies used by market leaders.

SmartChoiceGuide – Helpful content, making evaluating options straightforward and practical.

SkillBoostOnline – Provides practical resources that feel easy to follow and apply.

business trust resources – Hub provides clarity, forming meaningful relationships is easy.

directional progress – Helpful advice, shows how focused planning drives growth effectively.

next frontier commerce – Suggests exploring new business approaches and innovative retail solutions.

savvybusinesstips – Clear and useful, business advice is simple and effective.

alliances knowledge base – Structured insights, helps make sense of market partnership dynamics.

cross-border shopping hub – Concept supports smooth operations for international retail transactions.

SimpleEcommerceZone – Browsing products feels intuitive and hassle-free.

EnterpriseStrategyLink – Suggests a clear path for building effective partnerships.

valuealliances – Provides actionable insights for creating trustworthy and effective collaborations.

shopping variety zone – Nice mix of products that encourages looking around.

ecommerceportal – Clear and simple, the online purchase process is easy to follow.

online savings hub – Comfortable browsing experience with easy checkout and transparent pricing.

BuildSmartFuture – Supports structured strategic planning without overwhelming new users.

TrustedMarketHub – Reliable and easy to use, online shopping is hassle-free and safe.

global collaboration guide – Clear information, site feels intuitive for learning about partnerships.

futurebizplanner – Inspires thoughtful strategy, perfect for planning growth steps ahead.

learning clarity tips – Great resources, learning is simplified and actionable.

trustedtraderhub – Strong sense of trust, ideal for buyers seeking secure transactions online.

trusted alliance resources – Informative content, helps relate alliances to practical business cases.

GlobalShoppingOnline – Reliable platform, international buying is simple and user-friendly.

corporategrowthframeworks – Professional advice, frameworks are explained in a practical, step-by-step manner.

smartvaluepicks – Effortless way to locate daily bargains and value purchases.

Smart E-Shopping Center – Easy to navigate and full of useful advice for online purchases.

marketrelationshipsolutions – Very clear, guidance on market relationships is easy to follow and apply.

Career Growth Insights – Practical tips that help me develop professionally step by step.

securecommercialalliances – Feels safe and reliable, guidance on alliances is clear and actionable.

CustomerFirstClick – Smooth navigation and simple shopping process for all users.

EntrepreneurInsight – Encourages careful evaluation of emerging business opportunities.

growth mindset hub – Practical advice, long-term improvement is easier to visualize here.

trusted marketplace – Design feels reliable and browsing is effortless.

everyday items online – Easy navigation and responsive site make finding essentials simple.

NextLevelStrategy – Practical insights, step-by-step strategies are easy to implement.

alliances insight platform – Useful tips, simplifies how alliances operate in different markets.

safetraderhub – Marketplace feels safe and structured, encouraging buyers to make confident purchases.

motion mastery – Very practical, guidance makes building momentum easier.

ValueCartOnline – Designed to make online shopping practical and budget-friendly.

LearningForGrowth – Clear insights, helps you plan business expansion effectively.

everydaydealportal – Simple and practical, locating discounts online is easy and efficient.

Digital Growth Lab – Informative content with actionable tips for online growth strategies.

shopcityzone – Modern shopping hub with smooth navigation and simple checkout experience.

successinsights – Useful guidance, growth concepts are presented in a clear, step-by-step manner.

Smarter Pathways – Liked how the content broke complex ideas into usable steps.

ClickSmartBusiness – Helpful guides that are clear, concise, and ready to implement.

ProfessionalCredibilityNetwork – Trust-focused approach ensures confidence in developing long-term alliances.

online strategy roadmap – Practical layout, instructions simplify building digital skills.

market alliance insights – Helpful tips, shows how alliances work in realistic settings.

innovative ideas hub – Encourages approaching topics in a different, inspiring way.

corporateallianceshub – Feels solid and dependable, designed for professional networking and strategic connections.

bondadvisor – Useful and clear, commercial bond strategies are structured for real-world application.

frameworknavigator – Helps you apply structured growth methods in everyday business decisions.

BudgetFriendlyCart – Designed to attract shoppers who prioritize value and savings.

Business Connections – The information shared here is valuable and helps build meaningful professional links.

PlanYourFuturePortal – Supports structured and goal-oriented strategic thinking for businesses and individuals.

ScaleAndLearnPortal – Clear explanations, really helps in understanding expansion strategies.

learning expansion click – Content is approachable, gaining new knowledge feels effortless.

market alliance insights – Helpful tips, shows how alliances work in realistic settings.

Discover Market Insights – Content is easy to follow and practical for applying in real situations.

globalenterprisealliances – Informative platform, global alliance strategies are explained clearly and practically.

corporate confidence network – Emphasizes reliable business interactions, ideal for enterprises seeking long-term alliances.

BusinessSenseGuide – Practical tips that make learning business ideas easy.

scalepath – Clear guidance, growth strategies are broken down in a simple, actionable format.

reliable bargains hub – Comparing deals is quick, and the layout feels user-friendly and efficient.

digitalstrategycenter – Guidance is clear, making digital growth planning simple and actionable.

goal navigator – Very helpful, demonstrates how to focus energy in productive directions.

PremiumBuyHub – Sleek and reliable, shopping feels smooth and products are easy to find.

Future Commerce Ideas – The concepts feel modern and are explained in a way that’s simple to put into practice.

uncover options – Enjoyable approach, it makes discovery feel spontaneous.

FlexiBuyPortal – Provides a smooth and adaptable experience for online buyers.

SmartShoppingEcosystem – Clean design and easy browsing, learning about online retail is straightforward.

business alliance insights – Easy-to-follow advice, examples feel very relevant to real markets.

BizTrustLink – Encourages dependable partnerships among corporate entities.

strategy learning portal – Clear explanations, strategic concepts are approachable and simple.

GlobalOnlineBuyingHub – Found this resource valuable, explanations are concise and easy enough.

secureshopclick – Clear focus on safety, makes shopping feel risk-free and convenient.

EliteConnectionHub – Simple to navigate, encourages professional connections and trustworthy communication.

sustainablealliances – Practical guidance, strategies for eco-friendly business partnerships are simple and effective.

shopdailyonline – Simple and intuitive, online shopping feels smooth and hassle-free.

networking insights hub – Information is presented confidently and organized for seamless professional use.

growth focus tools – Practical insights, helps maintain focus while progressing steadily.

modern retail experience – Layout is clean and keeps visitors engaged while shopping.

SmartPlanPortal – Offers structured guidance for strategic planning while keeping objectives transparent and focused.

ClickTrustedEnterprise – Well-organized content, advice is actionable and reliable.

Enduring Partnership Lab – Practical guidance for keeping business relationships strong over time.

SmartMarketHub – Easy-to-follow content, market insights are structured and useful.

alliances knowledge base – Structured insights, helps make sense of market partnership dynamics.

StrategicBusinessAlliances – Solid website with practical tips I can apply immediately today.

discover partnership strategies – Clear explanations, guides for alliances are user-friendly and informative.

fastbuycenter – Clear and helpful, shopping online feels seamless.

ValueShopHub – Highlights savings, ideal for shoppers looking for the best deals online.

MegaDeals – Smooth interface, finding and buying items is quick and effortless.

trustedsalesportal – Professional look and feel, ensures peace of mind while shopping online.

commerceworldguide – Useful resource, international retail trends are clearly explained and actionable.

educational source – Keeps learning interesting while staying easy to follow.

StrategicBondPro – Structured and accurate, the content makes strategic bonds easy to follow.

PremiumOnlineBuyingHub – Well organized content that supports smarter decisions and planning efforts.

worldwide shopping portal – Diverse product range, easy to browse and purchase quickly.

StrategicPartnerLinks – Designed for professional alliances, prioritizing practical collaboration online.

DecisionSupportClick – Easy navigation and clear advice for evaluating different alternatives.

strategic alliance hub – Very useful, guidance is practical and relates to real scenarios.

ImpactSignal – Offers steps that convert effort into meaningful outcomes efficiently.

Retail Innovation Space – Offers detailed analysis and insights into the latest commerce trends.

trusted connections click – Content is approachable, forming alliances feels effortless.

visit yavlo – Pages load quickly, information is presented clearly and logically

ProfessionalTrustCenter – Reliable and clear, supports building trust in professional networks.

trustednetwork – Clear and user-friendly, guidance on forming professional alliances is presented logically.

OnlineGrowthBlueprint – Offers useful steps for building digital success efficiently.

international trade connections – Branding makes global networking feel approachable and actionable.

skillenhancementcenter – Helpful and well-structured, learning guidance is actionable and straightforward.

secure shopping hub – Professional and reassuring, perfect for repeat online buying.

Growth Strategy Lab – Excellent resource, provided clear steps and simplified decision-making.

zixor.click – Nice layout, loads quickly, information feels clear and useful today

ReliableBuyPlatform – Platform presents a secure and organized shopping experience for users.

trusted alliance resources – Informative content, helps relate alliances to practical business cases.

TrustedPurchaseHub – Well-organized platform, navigation is easy and content is useful.

Opportunity Discovery – Reading through this gave me new angles on potential ventures.

SmartDealsHub – Offers a platform for shoppers seeking the best value purchases.

professional unity tips – Content is detailed, site makes strategic connections easier.

bond basics hub – Makes enterprise bond information accessible and understandable for beginners.

top resource – Well-organized sections, readable content, interface is smooth

streamlined shopping – Excellent design, online purchases are simple and efficient.

valuefinder – Very user-friendly, discovering deals is quick and simple.

TopBargainSpot – Easy navigation, shopping for deals online is smooth and enjoyable.

CommercialLinkSafe – Platform inspires confidence, business operations are simple and secure.

securebuyzone – Marketplace feels professional, inspires confidence for first-time shoppers.

Business Path Finder – Clean interface and helpful insights make finding new strategies simple.

knowledgefromexperts – Very useful, insights from professionals are presented in a clear and approachable way.

international shopping hub – Offers a wide selection, appealing to buyers from many countries.

market collaboration hub – Informative advice, alliances explained clearly for market applications.

CollaborationNetworkPro – Highlights corporate teamwork and partnership opportunities in a clear format.

explorebusinessopportunities – Insightful resources, finding business opportunities feels easy and practical here.

WorldwideBizClick – Informative and concise, helps understand international business relationships.

Trusted Business Network – Practical tips that help strengthen credibility and relationships in the professional world.

start here – Fast and clean experience, navigation felt natural

partnershipinsights – Very clear, corporate alliance guidance is actionable for users.

nextlevel shop – Great platform, browsing products feels effortless and enjoyable.

StrategicAllianceGuide – Engaging content, helps plan alliances that are sustainable and effective.

SmartCartHub – Fast and clear, buying products online is safe and convenient.

SavvyDealsHub – Focuses on affordability and convenience for online buyers.

GlobalDigitalShoppingMarket – Really useful site, content feels practical and easy to navigate.

new enterprise paths – Encourages exploring alternative routes for business development today.

strategicbondnavigator – Offers structured tips for managing strategic bonds safely.

corporate network site – Suggests credibility and strong focus on serious business partnerships.

proinsightsmarketleaders – Helpful guidance, market leader strategies are presented in a clear, actionable format.

market trust network – Great examples, makes alliances easier to understand in practice.

CorporateGrowthLinks – Emphasizes durable corporate relationships that foster long-term opportunities.

UrbanShoppingClick – Smooth and practical, browsing product options is fast and effortless.

traction for progress – Clear and motivating, highlights how traction creates steady forward movement.

framework concepts portal – Clear organization and explanation make business concepts easy to follow.

Online Purchase Lab – Offers concise advice for navigating online stores efficiently.

go to site – Simple design, responsive pages, information is easy to follow

teaminsights – Very useful, professional collaboration guidance is actionable and easy to apply.

Discover Practical Ideas – Provides actionable tips with clear explanations for daily use.

EasyCartOnline – Shopping is convenient, platform layout is clear and organized.

insightful guides – Great tips, simplifies complex ideas for easy understanding.

resource page – Simple headings, readable content, pages are easy to move through

opportunity exploration hub – Promotes thinking beyond the short term to maximize potential.

smartshopbuilder – Appears user-friendly, great for entrepreneurs who want a no-fuss ecommerce launch.

ReliableCartCenter – Simple and clear, shopping online is quick and reliable.

trustedshopguide – The site ensures a secure, simple, and hassle-free shopping experience.

alliances resource center – Helpful guidance, simplifies understanding of market partnerships.

trustedconnections – Informative and professional, the advice on building market trust is straightforward.

InsightProNetwork – Focused on delivering real-world knowledge that professionals can implement easily.

ExpertStrategyHub – Very informative, helps translate expert advice into real-world action.

constructive momentum – Concise and encouraging, linking intentional effort to measurable forward action.

]bizlink – Helpful and straightforward, enterprise alliances are described clearly for practical use.

ValueCartOnline – Designed to make online shopping practical and budget-friendly.

start browsing – Navigation felt intuitive and the site felt polished overall

Everyday Buy Hub – The experience is clean and comfortable for regular use.

globaldigitalshoppingmarket – Smooth interface, site offers a good overview of digital marketplaces worldwide.

ModernRetailBuyingHub – Enjoyed browsing here, ideas are fresh and well explained clearly.

enhanced shopping portal – Navigation flows nicely across different product options.

BusinessSkillsMadeEasy – Informative platform, provides tools to develop real business competencies.

business mastery online – Shows the convenience of gaining business expertise remotely.

secure shopping hub – Helpful platform, checkout is fast and gives peace of mind.

businessboost – Clear, actionable advice to help your business thrive.

skill enhancement hub – Practical and well-organized way to strengthen personal and professional abilities.

decisionadvisorycenter – Clear strategies and tips for better choices in all situations.

SimpleClickShop – Offers straightforward digital shopping with minimal steps.

CorporateConnectionsPro – Well-organized platform, networking feels reliable and professional.

partnerstrategies – Concise and actionable, explains how to manage and build strategic alliances successfully.

GlobalTrustRelationshipNetwork – Clean layout and thoughtful content make this site enjoyable today.

cavlo.click – Found this by accident and liked how clean the page is

online portal – Fast-loading layout, readable pages, overall browsing is pleasant

NextGen E-Commerce Hub – Offers practical ways to discover products and make quick purchases.

momentum launch pad – Encouraging content makes starting feel less intimidating.

business partnership portal – Appears useful for companies exploring cooperative growth paths.

enterprisepathway – Practical methods to apply frameworks that enhance growth and collaboration.

greenselectionhub – Guides users to buy products that align with environmental responsibility.

BudgetSmart – Well-organized listings and useful info make comparison simple.

commercialallianceszone – Smooth and clear, commercial alliances guidance feels secure and actionable.

SmartShopCenter – Projects reliability and good value for online purchases.

CityRetailSpot – Compact and urban-focused, it gives a unique shopping experience for city users.

FocusedBusinessClick – Clear and practical advice that improved my decision-making.

ShopEaseOnline – Practical tips made my buying process smoother and faster.

EnterpriseFrameworkCenter – Well-organized content, concepts are easy to comprehend and apply.

connect smart professionally – Hub is informative, advice makes professional networking simpler.

useful link – Clean interface, smooth experience, information is easy to digest

TrustedCorporateNetwork – Clear and professional guidance, platform inspires confidence in corporate bonding.

Business Relationship Center – Helpful tips for creating dependable and effective business networks.

company alliance resource – Presents solutions aimed at strengthening enterprise relationships.

innovation strategies portal – Encourages trying new solutions rather than relying on old habits.

ventureweb – Guides you through the essentials of professional network building.

modern shopping hub – Sleek layout makes browsing smooth and shopping easy throughout.

reliableonlinecommerce – Safe and reliable, buying products online feels simple and secure today.

discover untapped markets – Inspires targeting unexplored areas with potential for innovation and profit.

vyrxo online – Clean interface, clear sections, and content flows nicely from page to page

SmartCartEcosystem – Buying approach emphasizes efficiency and thoughtful consumer choices.

longtermbizconnections – Helpful guidance, forming business relationships feels clear and manageable.

framework insights – Useful guidance, explains complex concepts clearly and efficiently.

explore signalturnsaction – Design is simple yet effective, everything is easy to find

FindSmarterBusinessMoves – Found this resource valuable, explanations are concise and easy enough.

tavro online – Clean interface, information is clear, and pages respond quickly

online portal – Fast-loading layout, readable pages, overall browsing is pleasant

alliances insight portal – Informative and structured, content clarifies international collaborations.

visit quvix – Smooth browsing experience, everything loads quickly and clearly

affordable deals hub – Appears targeted for savings, great for bargain-minded customers.

Strategy Inspiration – Plenty of useful thoughts that motivate experimenting with different methods.

WorldwideTrustGuide – Clear and actionable, networking globally is easy to manage.

BudgetWiseShop – Projects savings and reliability for online consumers.

partnershipsforfuture – Clear methods for creating sustainable and impactful business collaborations.

online buying support – Checkout is straightforward and builds confidence.

LearnFutureFocusedSkills – Solid website with practical tips I can apply immediately today.

BusinessClarityPortal – Provides guidance for making clear and confident decisions in complex business situations.

fast track purchases – Highlights quick and convenient options for completing orders.

visit zylor – Pleasant browsing experience, content is clear and well organized

focusamplifiesgrowth hub – Minimal clutter, structured content, and quick page loading

click for advanced strategies – Learning advanced tactics feels natural, explanations are simple and logical.

ShopQuickly – Easy navigation and smooth checkout make shopping a breeze.

click here – Clear design, smooth interface, easy to read content quickly

digital store solutions – Easy setup, seems well-suited for small business owners.

korixo web – Clear navigation and a friendly overall structure

Strategic Alliance Center – Very useful lessons on fostering partnerships that stand the test of time.

PlanYourStrategy – Helpful resources, strategic planning becomes approachable and effective.

BondInsightPro – Easy to follow, gave me a solid understanding of options.

OnlinePurchaseSafe – Security focus reassures users and encourages consistent engagement.

long-term growth strategies – Promotes forward-thinking approaches for enduring business success.

globalpartnershipinfrastructure – Very detailed, global partnership infrastructure is explained clearly and practically here.

growthflowswithclarity today – Pleasant layout, fast response, and content is concise yet informative

visit axivo – Well-organized pages, content is accessible and straightforward

go to site – Quick load times, simple design, content feels approachable

thrifty shopping hub – Value-oriented design, could help users find smart purchase options.

product site – Payment went smoothly, and I appreciated the shipping notifications.

Business Relationship Hub – Provides actionable tips for building and sustaining corporate bonds.

PurchaseHelper – Made understanding options quick and painless.

online shop hub – Well-structured navigation, and products appear authentic.

VisionaryRoutes – Encourages strategic foresight and creative consideration of future paths.

safetraderhub – Marketplace feels safe and structured, encouraging buyers to make confident purchases.

mexto source – Easy-to-read pages with information presented clearly

mavix portal – Smooth interface, information straightforward and browsing went without hiccups.

access progressmovesforwardnow – Layout feels intuitive, content is easy to find, and browsing is simple

xavro web – Simple design, readable content, and pages load quickly without clutter

online access – Pages open fast, layout is simple, content feels organized

smart shopping site – Clear value orientation, great for shoppers looking for savings.

storefront – Items were easy to browse, filtering helped me find what I needed fast.

Pelixo Network – Layout simple, pages open quickly and browsing feels intuitive.

NextGenOnlineBuying – Nice experience overall, navigation works smoothly and loads quickly everywhere.

Clear Path Growth – Guides me through options logically, removing uncertainty.

Visit Voryx – Layout straightforward, content easy to follow, and browsing was smooth.

BrixelPortal – Smooth experience, clear design, and moving between pages was effortless.

Ulvaro Select Shop – Navigation intuitive, pages organized and checkout completed without issues.

online retailer – Just discovered this site, fair deals and a simple checkout experience.

Kavion Path Market – Navigation easy, content well-structured and pages open quickly.

IntentionalStrategyHub – Offers focused guidance for cultivating strategic knowledge and professional growth.

QelaroGo – Accessible design that anyone can understand.

trustedcommercialbonds.click – Appears credible, could be useful for secure commercial bond transactions online.

official progressmoveswithfocus – Messaging is clear, with content presented in a logical order

quick link – Pages load quickly, layout is clear, impression is favorable

explorefuturedirections – Inspiring content, learning about future directions feels engaging and useful today.

clyra homepage – Thoughtful design, easy-to-navigate pages, and pleasant user experience

trusted corporate platform – The emphasis on integrity could draw in careful enterprises.

Yaveron Base – Layout intuitive, pages responsive and products easy to browse.

shopping platform – Feels dependable, product pages load fast, and buying is hassle-free.

ProfessionalBondSolutions – Great platform overall, information is clear and genuinely helpful today.

brivox access – No lag when opening pages, and the text remains clear

Korivo Click – Navigation effortless, content loads fast and product info reliable.

Online Shopping Tips Hub – Makes choosing the right products online simpler and faster.

online store – Fast loading, well-organized sections, and overall navigation is smooth.

Visit Vixor – Layout clean, content clear, and checkout went smoothly without issues.

Plivox Central – Minimal design, browsing smooth and checkout process hassle-free.

shop navix – Fast loading, simple checkout and navigation felt intuitive.

EffectiveSolutionsLab – Encourages strategies that are realistic, actionable, and results-oriented.

Mivaro Base – Fast loading, simple design and product details easy to find.

businesstrustcenter – Feels well-organized, highlighting trustworthy relationships for professionals.

PortalRixar – Layout clear, links worked correctly, and pages loaded without delays.

directionanchorsprogress destination – Well-structured layout, easy-to-understand content, and simple navigation overall

trusted link – Minimalist design with reliable navigation, everything functions well

corporate cooperation hub – Implies strong collaborative potential for enterprises worldwide.

plexin link – Straightforward layout, minimal distractions, and content flows nicely

shopping site – The delivery came carefully packed and on time.

Zorivo Hub World – Pages open quickly, layout intuitive and content easy to read.

zylavostore hub – Clean interface, product visuals sharp and details well presented.

Explore Business Strategies – The content nudged me to explore options outside my usual plans.

Velro Portal – Pages responsive, product details clear and overall experience smooth.

BondZexon – Clear descriptions, easy to compare items, and overall experience smooth.

Qulavo Flow Direct – Navigation straightforward, product info accurate and checkout works fine.

Zylavo Connect – Smooth interface, everything logically placed, and searching for products was simple.

online access – Pages respond quickly, simple design, very user-friendly

retail marketplace hub – Contemporary feel highlights current trends in retail buying.

directionpowersmovement site – Crisp design, easy-to-read content, and browsing feels seamless

xavix access – Professional feel, easy-to-use interface, and smooth site experience

purchase page – Mobile-friendly design, and categories are easy to browse.

tekvo destination – Simple interface, clear headings, and information is easy to find quickly

PlavexFlow – Smooth interface, fast pages, and site navigation feels natural.

SmartDailyPurchase – Easy and practical, completing online purchases is hassle-free.

Kryvox Zone – Site opened fast, content clear and finding products was straightforward.

Xelarionix Select – Fast loading, layout clear and content structured for easy reading.

xelarion store – Checked quickly, seems authentic and site layout is clean.

nolra online store – Layout clear, pages responsive and filtering makes selection easy.

Market Wisdom Center – Practical insights that make industry trends clearer and easier to follow.

Xelra Network – Browsing effortless, content well presented and shopping experience reliable.

Zaviro Express – Pages responsive, browsing easy, and completing orders was straightforward.

go to site – Quick response, intuitive structure, and content is well organized

modern e-commerce hub – Sleek design shows the current trends in online shopping preferences.

brand shop – The reply I received was professional and kind.

actionpowersmovement platform – Smooth experience, minimal clutter, and information is easy to digest

Morix Edge – Pages open efficiently, layout organized and shopping experience smooth.

official axory – Simple interface, fast-loading pages, and smooth browsing throughout

LinkStream – Pages responded fast, information appeared relevant.

zorivo main site – Pages opened instantly, layout straightforward and sections clear.

Rixaro Express – Pages responsive, navigation smooth and overall shopping experience reliable.

olvra destination – Quick access with neat structure and reliable content throughout

Business Relations Hub – Everything is laid out nicely, making global networking straightforward.

MorixoNavigator – Clean layout, pages load quickly, and finding items feels natural.

Kryvox Online Shop – Layout simple, content clear and purchasing process effortless.

torivo market – The website looks clean, products are decent, and checkout went smoothly.

click here – Simple navigation, fast performance, content is easy to understand

Kelvo Main – Pages loaded quickly, navigation intuitive and overall shopping felt effortless.

NevironLink – Pages opened without errors, layout logical, and site felt safe to use.

ideasbecomeforward info – Fast loading, organized pages, and content is presented in a user-friendly way

check olvix – Clean pages, intuitive structure, and information is simple to follow

nexlo shop hub – Quick-loading pages, easy to order and overall experience satisfying.

product marketplace – Listings are clear and easy to navigate, and filtering worked perfectly today.

Pelix Central – Fast loading, product info clear and overall shopping experience straightforward.

SafeDealNetwork – Trustworthy platform, locating and purchasing deals is convenient.

Qulavo Online – Navigation intuitive, content well-organized and purchasing process hassle-free.

Korla Online Shop – Pages load quickly, layout simple and checkout felt effortless.

marketplace – Found this while browsing and added it to my list.

Korva Resource – Came across this casually, the presentation is fresh and readable

check actioncreatesforwardpath – Easy-to-follow structure, readable information, and site feels professional

nolix info – Tidy layout and readable content make browsing effortless

Click Torix – Layout minimal, content easy to find, and purchasing steps straightforward.

QuickPrixoClick – Responsive pages, tidy design, and checkout process smooth.

XalorLink – Fast and smooth, all links functional, and site feels credible.

official klyvo – Simple interface, clear text, and smooth browsing experience

click portal – Fast checkout experience, confirmation arrived quickly afterwards.

Cavaro Live – Smooth experience, accurate content, and navigation simple to follow.

Visit Zexaro Forge – Pages responsive, layout clear and browsing felt effortless.

shopping site – The site is tidy, product details make sense, and pictures reflect the items well.

Zarix Network – Pages respond quickly, content organized and shopping flow feels natural.

browse qavrix – Simple, clear, and responsive pages make browsing comfortable

BusinessConnectionsOnline – Easy-to-follow content, understanding global business ties is simple.

focusdrivesmovement – Enjoyed visiting, everything loads fast and feels well organized overall

UlvaroShop – Pages load quickly, layout is neat, and product details are easy to read.

ClickEaseRixva – Fast pages, intuitive design, and finding items easy and quick.

Mivaro Spot – Content well organized, pages responsive and shopping steps easy to follow.

Brixel Trustee web page – The content is easy to read, and the site is intuitive to navigate.

Maverounity info site – Clean execution makes the project feel credible.

QuickXaneroClick – Pages responsive, interface neat, and content easy to explore.

zaviro portal – Clicked through without issues, page content made sense immediately.

Zavirobase Online – Smooth interface, pages load without delay and shopping feels seamless.

Kryvox Bonding landing page – Neat layout, easy-to-follow navigation, and trustworthy content throughout.

Morixo Trustee web portal – Pages load quickly, content is structured, and overall experience is reliable.

qavon destination – Pleasant and contemporary site design with clear, organized content

shopping site – I had no concerns during payment and the receipt was immediate.

Nolaro Trustee official site – Easy-to-read content, strong design, and the user experience is clear.

Learn about Qelaro Bonding – Smooth browsing, organized content, and pages are easy to navigate.

RelationshipInsightCenter – Helpful and actionable, building corporate networks feels straightforward.

Kryxo Hub Store – Minimal design, navigation smooth and ordering process worked without issues.

browse nixra – Fast response times and uncluttered layout, enjoyable to click around

ClickYavon – Interface intuitive, pages open smoothly, and all sections easy to navigate.

Zylra Storefront – Fast site, items easy to find and checkout felt reliable.

focusbuildsenergy online – Crisp pages, well-structured content, and the site feels professional

Cavaro Bonding official site – Clean design and trustworthy information make it feel professional.

OpportunityInsightHub – Clear and helpful, understanding long-term prospects is straightforward.

Zavix Online – Layout simple, information organized well, and completing purchases was easy.

redirect hub – Quick load times, link worked exactly as expected with no problems.

Ravion Bonded web portal – Information is presented clearly, with updates that feel consistent and useful.

Nixaro Point – Information clear, navigation simple and purchasing process effortless.

Kryvox Capital info site – Clean pages, logical navigation, and the content feels professional.

web shop – Layout is neat and simple, making the shopping experience smooth.

Nolaro Trustee official site – Easy-to-read content, strong design, and the user experience is clear.

Naviro Bonding business site – Well-laid-out pages, easy navigation, and content is easy to follow.

Qelaro Capital web – Easy-to-use interface, clean layout, and the site is easy to follow.

UlvionCenter – Pages opened quickly, interface professional, and information presented clearly.

Zexaro Central – Product info clear, pages responsive and navigation intuitive.

trusted hub – Everything functions smoothly, clean layout made it easy to browse

Zavro World – Site loads fast, content clear and overall experience reliable.

RavloPortal – Content is accurate, pages load quickly, and product details are clear.

Explore Cavaro Trust Group – Fast navigation and organized details make the platform simple to use.

signal guides growth link – Easy to navigate, concise content, and clear layout throughout

ravixo network – Pages load efficiently with text that is concise and informative

official page – Well-presented information, solid layout, and the idea behind the site is interesting.

BrixelPortal – Pages load quickly, layout intuitive, and browsing experience enjoyable.

InnovationExplorer – Clear and engaging lessons, new ideas are easy to understand.

Vixaro Point – Pages load quickly, layout intuitive and navigation feels seamless.

Cavix web platform – Simple menus and structure help users understand the purpose quickly.

retail website – Shipping methods were sensible, and arrival estimates were realistic.

Korivo Network – Pages opened quickly, navigation clear and content easy to read.

Check Pelixo Bond Group – Smooth interface, concise content, and information is easy to access.

Kryvox Trust main site – Quick load times, user-friendly navigation, and information is organized logically.

Qelaro Trustline hub – Fast pages, clear headings, and content is presented logically.

Naviro Capital landing page – Well-organized sections, quick navigation, and details are simple to find.

TrivoxGo – Fast redirect, content seemed reliable and navigation was seamless.

Velixonode Express Hub – Quick site response, content clear and overall experience pleasant and reliable.

Cavaro Union homepage – Visuals are well-aligned, brand messaging is steady, and the purpose comes across clearly.

visit signalactivatesgrowth – Layout is simple and intuitive, making it easy to find key information

ClickEase – Fast-loading pages, layout organized, and browsing is very straightforward.

NextGrowthHub – Clear and practical, growth ideas are easy to understand and use.

Xelivo Online Shop – Navigation simple, pages load quickly and checkout was hassle-free.

network page – Detailed security info reassured me while browsing through pages.

online retailer – The experience felt solid with no unexpected errors.

useful link – Intuitive layout, sections are concise and easy to browse

Naviro Trustee info site – The site’s structure makes key details easy to access.

Pelixo Capital landing page – Simple design, organized content, and navigation flows naturally.

QulixCenter – Simple navigation, quick loading, and shopping process feels intuitive and smooth.

Qorivo Bonding Info – User-friendly design, readable content, and browsing is smooth overall.

BondXpress – Pages load fast, design feels clean, and content is simple to navigate.

bryxo source – Natural-looking content and navigation that doesn’t get in the way

BuyOnlineNow – Modern interface, shopping online is smooth and straightforward.

Neviror Trust online portal – Clear layout, reliable content, and user experience is intuitive.

Kavion Bonding online site – Everything is arranged logically, communication is transparent, and the site feels reliable.

check directionunlocksgrowth – Neat interface, sections are easy to follow, and the site feels reliable

Pelixo Zone – Navigation effortless, product listings clear and overall experience pleasant.

information hub – Minimal styling, content is clear, and navigation feels effortless.

store page – Items are listed neatly, and filtering helped me focus on what I wanted.

trusted resource – Clear design, pages respond quickly, content is informative

Pelixo Trust Group network – Professional look, easy-to-scan content, and pages feel smooth to browse.

Mivon info site – The project feels promising thanks to its open presentation.

plixo online hub – Navigation simple, layout clean and checkout process seamless.

Kavion Trustee official site – Polished layout, noticeable credibility features, and smooth navigation throughout.

Visit Qorivo Holdings – Well-organized content, intuitive navigation, and overall browsing is smooth.

TorivoUnion Website – Straightforward and clear, gives a trustworthy long-term impression.

PortalQori – Well-organized content, pages load quickly, and overall site flow is intuitive.

Explore UlviroBondGroup – Discovered this, looks legit and details are easy to understand.

Neviro Union digital platform – Clean design, trustworthy feel, and navigation flows without effort.

Neviro Access – Layout neat, information accurate and overall shopping experience pleasant.

SecurePurchasePro – Fast and intuitive, shopping online is clear and hassle-free.

progressmovesintelligently access – Straightforward navigation, concise content, and smooth browsing experience

cavix link – Nice flow overall, the design stays simple while sharing good info

official portal – Fast and reliable, readable text, and site feels expertly crafted.

shop website – Easy-to-follow steps made checkout quick and hassle-free.

main brixo – Quick page loads, interface simple and ordering process seamless.

Qelix official site – The site is easy to use, with details presented cleanly and logically.

Xeviro Network – Pages load quickly, product info clear and buying process easy.

Qorivo Trustline Info – Well-arranged content, fast navigation, and interface feels user-friendly.

TrivoxBonding Hub – Spotted this while looking around, layout and info look solid.

FutureInsightsHub – Informative and clear, exploring upcoming trends feels simple and engaging.

ToriVoOnline – Layout professional, pages easy to navigate, and information clear and easy to read.

Nixaro Holdings digital platform – Clear structure, professional presentation, and finding information is effortless.

actiondrivesdirection corner – Readable text, clear headings, and pages are responsive overall

KnowledgeExpandPro – Very informative, learning new topics feels structured and approachable.

this shop – It looks like a legitimate site with information laid out clearly.

digital store – Everything is neatly arranged, reading info is easy, and navigation is straightforward.

kavion main site – Trust badges visible, product info clear and site overall reliable.

Morixo Direct – Pages open fast, navigation intuitive and shopping experience enjoyable.

Qulavo Bonding Online – Clear headings, organized content, and overall browsing is effortless.

Xaliro Drive online platform – Pages respond quickly, and the idea behind the platform feels engaging.

TrivoxCapital Page – Information is presented clearly, navigation doesn’t feel cluttered.

Visit Nixaro Partners – Well-laid-out pages, navigation is simple, and users can find info quickly.

Ulxra Center – Smooth navigation, product listings clear, and checkout process simple.

signalcreatesflow point – Organized content and smooth navigation make browsing pleasant

Zaviro Point – Layout neat, content loads fast and product selection easy to understand.

this online store – I appreciated how fast the site responded while exploring products.

QuickDecisionHub – Tips are concise, allowing users to make informed choices quickly.

ZexaroAccess – Minimalist pages, smooth navigation, and all content displayed clearly.

main portal – Fast load, destination accurate, link performed without any issues.

Plavex Capital site – Professional design, structured content, and finding information is easy.

Qulavo Capital Network – Clear headings, organized content, and pages are simple to browse.

globalenterprisealliances – Informative platform, global alliance strategies are explained clearly and practically.

TrivoxTrustline Info – Plenty of transparency shown, which helps build confidence.

Ulvix online hub – Concise explanations and a tidy layout improve readability.

UlviroCapitalGroup Platform – Simple design, well-structured pages and information is clear.

project page – Loads promptly and feels well put together overall

Kavion Trust Group online hub – Well-laid-out pages, clear messaging, and navigation feels effortless.

Explore Nixaro Trustline – Simple navigation, organized content, and trust elements are clear throughout.

Trivox Live – Navigation easy, pages responsive and product information clear.

KoriPortal – Design minimalistic, content readable, and purchasing process smooth.

focusanchorsmovement platform – User-friendly layout, information is easy to locate, and pages respond quickly

marketplace listing – The product text felt genuine and believable.

HoldingFlow – Fast response, structured content, and navigation is intuitive.

xeviro portal shop – Pleasant experience, consistent branding and details easy to find.

Learn about Plavex Holdings – Smooth interface, clear content, and navigating the site is straightforward.

zavik site – Information is presented clearly with a tidy, user-friendly interface

Visit this online platform – The design and wording give off a trustworthy, polished feel.

TrustMarketCenter – Easy to use, online buying is safe and efficient.

Explore Qulavo Capital – Clean design, clear sections, and overall experience is intuitive.

UlvaroBondGroup Main Site – Came across this today, layout is clean and communication is direct.

(10 euros gratis apuestas|10 mejores casas de apuestas|10 trucos para ganar apuestas|15 euros gratis

marca apuestas|1×2 apuestas|1×2 apuestas deportivas|1×2 apuestas que significa|1×2

en apuestas|1×2 en apuestas que significa|1×2 que significa en apuestas|5 euros gratis apuestas|9 apuestas que siempre ganaras|a partir

de cuanto se declara apuestas|actividades de juegos de azar y apuestas|ad apuestas deportivas|aleksandre topuria ufc

apuestas|algoritmo para ganar apuestas deportivas|america apuestas|análisis nba apuestas|aplicacion android apuestas deportivas|aplicacion apuestas deportivas|aplicacion apuestas deportivas android|aplicación de apuestas online|aplicacion para hacer

apuestas|aplicacion para hacer apuestas de futbol|aplicación para hacer apuestas

de fútbol|aplicaciones apuestas deportivas android|aplicaciones apuestas deportivas gratis|aplicaciones de apuestas android|aplicaciones de

apuestas de fútbol|aplicaciones de apuestas deportivas|aplicaciones de apuestas deportivas peru|aplicaciones de apuestas deportivas

perú|aplicaciones de apuestas en colombia|aplicaciones

de apuestas gratis|aplicaciones de apuestas online|aplicaciones de

apuestas seguras|aplicaciones de apuestas sin dinero|aplicaciones para hacer apuestas|apostar

seguro apuestas deportivas|app android apuestas deportivas|app apuestas|app apuestas

android|app apuestas de futbol|app apuestas deportivas|app apuestas

deportivas android|app apuestas deportivas argentina|app apuestas deportivas colombia|app apuestas deportivas ecuador|app

apuestas deportivas españa|app apuestas deportivas gratis|app apuestas entre amigos|app

apuestas futbol|app apuestas gratis|app

apuestas sin dinero|app casa de apuestas|app casas de apuestas|app control apuestas|app de apuestas|app de

apuestas android|app de apuestas casino|app de apuestas colombia|app de apuestas con bono de bienvenida|app de apuestas de futbol|app de apuestas deportivas|app de apuestas deportivas android|app de apuestas

deportivas argentina|app de apuestas deportivas

colombia|app de apuestas deportivas en españa|app de apuestas deportivas peru|app de

apuestas deportivas perú|app de apuestas deportivas sin dinero|app de apuestas ecuador|app de apuestas en colombia|app

de apuestas en españa|app de apuestas en venezuela|app de apuestas futbol|app de apuestas gratis|app de apuestas online|app

de apuestas para android|app de apuestas para ganar dinero|app de apuestas

peru|app de apuestas reales|app de casas de apuestas|app marca apuestas android|app moviles de

apuestas|app para apuestas|app para apuestas de futbol|app para apuestas

deportivas|app para apuestas deportivas en español|app para

ganar apuestas deportivas|app para hacer apuestas|app para hacer

apuestas deportivas|app para hacer apuestas entre amigos|app para llevar control de apuestas|app

pronosticos apuestas deportivas|app versus apuestas|apps apuestas

mundial|apps de apuestas|apps de apuestas con bono de bienvenida|apps de apuestas

de futbol|apps de apuestas deportivas peru|apps de apuestas mexico|apps para apuestas|aprender a hacer apuestas deportivas|aprender hacer apuestas deportivas|apuesta del dia apuestas deportivas|apuestas 10

euros gratis|apuestas 100 seguras|apuestas 1×2|apuestas 1X2|apuestas 2 division|apuestas 3 division|apuestas a caballos|apuestas

a carreras de caballos|apuestas a colombia|apuestas

a corners|apuestas a ganar|apuestas a jugadores nba|apuestas a la baja|apuestas

a la nfl|apuestas al barcelona|apuestas al

dia|apuestas al empate|apuestas al mundial|apuestas al tenis wta|apuestas alaves barcelona|apuestas alcaraz hoy|apuestas

alemania españa|apuestas alonso campeon del mundo|apuestas

altas y bajas|apuestas altas y bajas nfl|apuestas ambos equipos marcan|apuestas

america|apuestas android|apuestas anillo nba|apuestas antes del mundial|apuestas anticipadas|apuestas anticipadas nba|apuestas apps|apuestas arabia argentina|apuestas argentina|apuestas argentina campeon del mundo|apuestas argentina canada|apuestas argentina colombia|apuestas argentina croacia|apuestas argentina españa|apuestas

argentina francia|apuestas argentina francia cuanto paga|apuestas argentina

francia mundial|apuestas argentina gana el mundial|apuestas argentina gana mundial|apuestas argentina holanda|apuestas argentina

mexico|apuestas argentina méxico|apuestas argentina mundial|apuestas argentina online|apuestas argentina

paises bajos|apuestas argentina polonia|apuestas argentina

uruguay|apuestas argentina vs australia|apuestas argentina vs colombia|apuestas argentina vs francia|apuestas argentina vs peru|apuestas argentinas|apuestas arsenal real madrid|apuestas ascenso a primera division|apuestas ascenso a segunda|apuestas asiaticas|apuestas asiatico|apuestas athletic|apuestas athletic atletico|apuestas athletic barça|apuestas athletic barcelona|apuestas athletic betis|apuestas athletic manchester|apuestas athletic manchester united|apuestas athletic osasuna|apuestas

athletic real|apuestas athletic real madrid|apuestas athletic real sociedad|apuestas athletic real sociedad final|apuestas athletic roma|apuestas athletic sevilla|apuestas athletic

valencia|apuestas atletico|apuestas atletico barcelona|apuestas atletico barsa|apuestas atletico campeon champions|apuestas atletico campeon de liga|apuestas atlético copenhague|apuestas atletico de madrid|apuestas atlético de madrid|apuestas atletico de madrid

barcelona|apuestas atletico de madrid gana la liga|apuestas atletico de madrid real madrid|apuestas

atlético de madrid real madrid|apuestas atletico de madrid vs barcelona|apuestas atletico

madrid|apuestas atletico madrid real madrid|apuestas

atletico madrid vs barcelona|apuestas atletico real

madrid|apuestas atletico real madrid champions|apuestas atletismo|apuestas bajas|apuestas baloncesto|apuestas

baloncesto acb|apuestas baloncesto handicap|apuestas baloncesto hoy|apuestas baloncesto juegos olimpicos|apuestas baloncesto nba|apuestas baloncesto pronostico|apuestas baloncesto pronósticos|apuestas baloncesto prorroga|apuestas barca|apuestas barca athletic|apuestas barca

atletico|apuestas barca bayern|apuestas barca bayern munich|apuestas barca girona|apuestas barca hoy|apuestas

barça hoy|apuestas barca inter|apuestas barca juventus|apuestas barca madrid|apuestas barça madrid|apuestas barca real madrid|apuestas barca vs juve|apuestas barca vs madrid|apuestas barca vs psg|apuestas

barcelona|apuestas barcelona alaves|apuestas barcelona athletic|apuestas

barcelona atletico|apuestas barcelona atletico de madrid|apuestas barcelona atlético

de madrid|apuestas barcelona atletico madrid|apuestas barcelona bayern|apuestas barcelona betis|apuestas barcelona campeon de liga|apuestas barcelona celta|apuestas barcelona espanyol|apuestas barcelona gana la champions|apuestas

barcelona girona|apuestas barcelona granada|apuestas barcelona hoy|apuestas barcelona

inter|apuestas barcelona madrid|apuestas barcelona

osasuna|apuestas barcelona psg|apuestas barcelona real madrid|apuestas barcelona real sociedad|apuestas

barcelona sevilla|apuestas barcelona valencia|apuestas barcelona villarreal|apuestas barcelona vs atletico

madrid|apuestas barcelona vs madrid|apuestas barcelona vs

real madrid|apuestas barsa madrid|apuestas basket hoy|apuestas bayern barcelona|apuestas bayern vs barcelona|apuestas

beisbol|apuestas béisbol|apuestas beisbol mlb|apuestas beisbol pronosticos|apuestas beisbol venezolano|apuestas

betis|apuestas betis – chelsea|apuestas betis barcelona|apuestas betis chelsea|apuestas betis fiorentina|apuestas betis girona|apuestas betis madrid|apuestas betis mallorca|apuestas betis real madrid|apuestas betis real sociedad|apuestas betis sevilla|apuestas betis valencia|apuestas

betis valladolid|apuestas betis vs valencia|apuestas betplay hoy colombia|apuestas betsson peru|apuestas bienvenida|apuestas billar online|apuestas bolivia vs colombia|apuestas bono|apuestas bono bienvenida|apuestas bono de bienvenida|apuestas bono de bienvenida sin deposito|apuestas bono gratis|apuestas bono sin deposito|apuestas bonos sin deposito|apuestas borussia real madrid|apuestas boxeo|apuestas boxeo de campeonato|apuestas boxeo españa|apuestas boxeo español|apuestas boxeo femenino

olimpiadas|apuestas boxeo hoy|apuestas boxeo online|apuestas brasil colombia|apuestas brasil peru|apuestas brasil uruguay|apuestas brasil vs

colombia|apuestas brasil vs peru|apuestas caballos|apuestas caballos colocado|apuestas caballos españa|apuestas

caballos hipodromo|apuestas caballos hoy|apuestas caballos

madrid|apuestas caballos online|apuestas caballos sanlucar de barrameda|apuestas

caballos zarzuela|apuestas calculador|apuestas campeon|apuestas campeon champions|apuestas campeón champions|apuestas campeon champions

2025|apuestas campeon champions league|apuestas campeon conference league|apuestas campeon copa america|apuestas campeon copa del rey|apuestas campeon de champions|apuestas

campeon de la champions|apuestas campeon de liga|apuestas campeon del

mundo|apuestas campeon eurocopa|apuestas campeón eurocopa|apuestas campeon europa league|apuestas campeon f1|apuestas campeon f1 2025|apuestas campeon formula 1|apuestas campeon libertadores|apuestas campeon liga|apuestas

campeon liga bbva|apuestas campeon liga española|apuestas campeon liga santander|apuestas campeon motogp 2025|apuestas campeon mundial|apuestas campeón mundial|apuestas

campeon mundial baloncesto|apuestas campeon nba|apuestas campeón nba|apuestas campeon premier|apuestas

campeon premier league|apuestas campeon roland garros|apuestas campeonato f1|apuestas campeonatos de

futbol|apuestas carrera de caballos|apuestas carrera de caballos hoy|apuestas

carrera de caballos nocturnas|apuestas carrera de galgos

fin de semana|apuestas carrera de galgos hoy|apuestas carrera de galgos

nocturnas|apuestas carreras caballos|apuestas carreras caballos sanlucar|apuestas carreras de caballos|apuestas carreras de caballos en directo|apuestas carreras de caballos en vivo|apuestas carreras de caballos españa|apuestas carreras de caballos hoy|apuestas carreras de caballos nacionales|apuestas carreras de caballos nocturnas|apuestas carreras de caballos online|apuestas carreras de

caballos sanlucar|apuestas carreras de caballos sanlúcar|apuestas carreras de galgos|apuestas carreras de galgos

en vivo|apuestas carreras de galgos nocturnas|apuestas

carreras de galgos pre partido|apuestas casino|apuestas casino

barcelona|apuestas casino futbol|apuestas casino gran madrid|apuestas casino gratis|apuestas casino madrid|apuestas casino online|apuestas

casino online argentina|apuestas casinos|apuestas casinos online|apuestas celta|apuestas celta barcelona|apuestas

celta betis|apuestas celta eibar|apuestas celta espanyol|apuestas celta granada|apuestas celta madrid|apuestas celta manchester|apuestas celta

real madrid|apuestas champion league|apuestas champions foro|apuestas

champions hoy|apuestas champions league|apuestas champions league

– pronósticos|apuestas champions league 2025|apuestas champions league hoy|apuestas champions league pronosticos|apuestas champions league pronósticos|apuestas champions pronosticos|apuestas chelsea barcelona|apuestas chelsea betis|apuestas chile|apuestas chile peru|apuestas chile venezuela|apuestas chile

vs colombia|apuestas chile vs uruguay|apuestas ciclismo|apuestas ciclismo en vivo|apuestas ciclismo femenino|apuestas ciclismo tour francia|apuestas ciclismo vuelta|apuestas ciclismo vuelta a españa|apuestas ciclismo vuelta españa|apuestas city madrid|apuestas city real madrid|apuestas clasico|apuestas clasico español|apuestas clasico real

madrid barcelona|apuestas clasificacion mundial|apuestas colombia|apuestas colombia argentina|apuestas colombia brasil|apuestas colombia paraguay|apuestas

colombia uruguay|apuestas colombia vs argentina|apuestas colombia vs brasil|apuestas combinadas|apuestas combinadas como funcionan|apuestas combinadas de futbol|apuestas combinadas

de fútbol|apuestas combinadas foro|apuestas combinadas futbol|apuestas combinadas hoy|apuestas combinadas

mismo partido|apuestas combinadas mundial|apuestas combinadas nba|apuestas combinadas para esta semana|apuestas combinadas para hoy|apuestas

combinadas para mañana|apuestas combinadas pronosticos|apuestas combinadas

recomendadas|apuestas combinadas seguras|apuestas combinadas seguras para

hoy|apuestas combinadas seguras para mañana|apuestas como ganar|apuestas comparador|apuestas con bono de bienvenida|apuestas con dinero ficticio|apuestas con dinero real|apuestas con dinero virtual|apuestas con handicap|apuestas con handicap

asiatico|apuestas con handicap baloncesto|apuestas con mas probabilidades de ganar|apuestas

con paypal|apuestas con tarjeta de credito|apuestas con tarjeta de

debito|apuestas consejos|apuestas copa|apuestas copa africa|apuestas copa

america|apuestas copa américa|apuestas copa argentina|apuestas copa

brasil|apuestas copa davis|apuestas copa de europa|apuestas copa del mundo|apuestas copa del

rey|apuestas copa del rey baloncesto|apuestas

copa del rey final|apuestas copa del rey futbol|apuestas copa del rey ganador|apuestas copa del

rey hoy|apuestas copa del rey pronosticos|apuestas copa del rey pronósticos|apuestas copa europa|apuestas copa italia|apuestas copa libertadores|apuestas copa mundial de hockey|apuestas copa rey|apuestas copa sudamericana|apuestas corners|apuestas corners hoy|apuestas croacia argentina|apuestas cuartos

eurocopa|apuestas cuotas|apuestas cuotas altas|apuestas cuotas bajas|apuestas de 1 euro|apuestas de baloncesto|apuestas de baloncesto hoy|apuestas de baloncesto

nba|apuestas de baloncesto para hoy|apuestas de beisbol|apuestas de beisbol para hoy|apuestas de blackjack en linea|apuestas de boxeo|apuestas de boxeo canelo|apuestas de boxeo en las vegas|apuestas de boxeo hoy|apuestas

de boxeo online|apuestas de caballo|apuestas de caballos|apuestas de

caballos como funciona|apuestas de caballos como se juega|apuestas de caballos en colombia|apuestas de caballos en españa|apuestas de caballos en linea|apuestas de caballos

españa|apuestas de caballos ganador y colocado|apuestas de caballos internacionales|apuestas de caballos juegos|apuestas de caballos online|apuestas de caballos online en venezuela|apuestas de caballos por internet|apuestas de caballos

pronosticos|apuestas de caballos pronósticos|apuestas de carrera de

caballos|apuestas de carreras de caballos|apuestas de carreras de caballos online|apuestas de

casino|apuestas de casino online|apuestas de casino por internet|apuestas de champions

league|apuestas de ciclismo|apuestas de colombia|apuestas de copa america|apuestas de corners|apuestas de deportes en linea|apuestas de deportes online|apuestas de

dinero|apuestas de esports|apuestas de eurocopa|apuestas de europa league|apuestas de f1|apuestas de formula 1|apuestas de futbol|apuestas de fútbol|apuestas de

futbol app|apuestas de futbol argentina|apuestas de futbol colombia|apuestas de futbol en colombia|apuestas de futbol en directo|apuestas de

futbol en linea|apuestas de futbol en vivo|apuestas de futbol

español|apuestas de futbol gratis|apuestas de futbol hoy|apuestas de futbol mundial|apuestas de futbol online|apuestas

de fútbol online|apuestas de futbol para hoy|apuestas de fútbol para hoy|apuestas de futbol para hoy seguras|apuestas de futbol para mañana|apuestas de futbol peru|apuestas de futbol pronosticos|apuestas

de fútbol pronósticos|apuestas de futbol seguras|apuestas de futbol seguras

para hoy|apuestas de futbol sin dinero|apuestas de galgos|apuestas de galgos como ganar|apuestas de galgos en directo|apuestas de galgos online|apuestas de galgos trucos|apuestas

de golf|apuestas de hockey|apuestas de hockey

sobre hielo|apuestas de hoy|apuestas de hoy seguras|apuestas de

juego|apuestas de juegos|apuestas de juegos deportivos|apuestas de juegos online|apuestas de la champions league|apuestas de

la copa américa|apuestas de la eurocopa|apuestas de la europa league|apuestas de la liga|apuestas de

la liga bbva|apuestas de la liga española|apuestas de la nba|apuestas de la nfl|apuestas de la ufc|apuestas de mlb|apuestas de nba|apuestas de nba para hoy|apuestas de partidos|apuestas de partidos de

futbol|apuestas de peleas ufc|apuestas de perros en vivo|apuestas de perros virtuales|apuestas de peru|apuestas de

sistema|apuestas de sistema como funciona|apuestas de sistema explicacion|apuestas de sistema explicación|apuestas de tenis|apuestas de tenis de mesa|apuestas de tenis en directo|apuestas

de tenis hoy|apuestas de tenis para hoy|apuestas de tenis pronosticos|apuestas de tenis seguras|apuestas

de todo tipo|apuestas de ufc|apuestas de ufc hoy|apuestas

del boxeo|apuestas del clasico|apuestas del clasico real

madrid barca|apuestas del dia|apuestas del día|apuestas del dia de hoy|apuestas del dia deportivas|apuestas del dia futbol|apuestas

del mundial|apuestas del partido de hoy|apuestas

del real madrid|apuestas del rey|apuestas del sistema|apuestas deporte|apuestas deportes|apuestas deportiva|apuestas deportivas|apuestas deportivas 1 euro|apuestas deportivas 10 euros gratis|apuestas deportivas